TL;DR:

- Roofing upgrades can lower insurance premiums by improving your home’s risk profile and qualifying you for discounts. Proper documentation of certifications and installation details is essential to trigger these savings, which may take several months to reflect after the upgrade. Consulting with an experienced agent and providing thorough records ensures you maximize financial benefits from your roof improvements.

Roofing upgrades directly affect insurance premiums by changing how insurers calculate your home’s risk profile, coverage eligibility, and claim payout potential. The industry term for this process is “underwriting adjustment,” and it happens every time your insurer updates its data on your roof’s age, condition, or material. Knowing how roofing upgrades affect insurance premiums gives you real leverage when it’s time to negotiate coverage or renew your policy. Older roofs can trigger surcharges of 10% to 20% or more, which means a well-timed upgrade is one of the most direct ways to control what you pay. This article breaks down exactly what insurers look at, how valuation methods shape your payout, and which upgrades deliver the strongest financial return.

How do insurers assess roof factors when determining premiums?

Insurers treat your roof as the single most consequential structural element on your home. It is the first line of defense against storm damage, leaks, and water intrusion, and those risks translate directly into claim frequency and severity. According to Verisk’s 2026 U.S. Roof Report, 38% of U.S. residential roofs show moderate to poor condition, and those roofs carry approximately 60% higher loss costs than roofs in good or excellent condition. That gap in loss cost is exactly why insurers price roof risk so aggressively.

Here are the primary factors underwriters evaluate when pricing your policy:

- Roof age. Most insurers begin applying surcharges once a roof passes 15 to 20 years. After 25 years, some carriers restrict coverage entirely. The California FAIR Plan, for example, restricts full replacement-cost coverage for roofs older than 25 years unless the roof has been replaced.

- Roof condition. Age alone does not tell the full story. A 12-year-old roof with hail damage and missing granules may be rated worse than a 20-year-old roof that has been well maintained. Insurers use aerial imagery analytics to assess condition remotely, which means your roof may already be flagged in their system before you file a single claim.

- Roofing material. Impact-resistant shingles, metal roofing, and Class 4 rated materials all reduce the probability of storm damage. Insurers reward lower-risk materials with lower base rates.

- Roof design and drainage. Hip roofs shed wind better than gable roofs. Proper gutters and drainage reduce water intrusion risk. Both factors influence the insurer’s overall risk score for your property.

Pro Tip: Before your next policy renewal, pull your roof’s installation records and share them directly with your insurer. Insurers relying on aerial data may have outdated or inaccurate condition scores, and a simple documentation submission can correct a surcharge you didn’t earn.

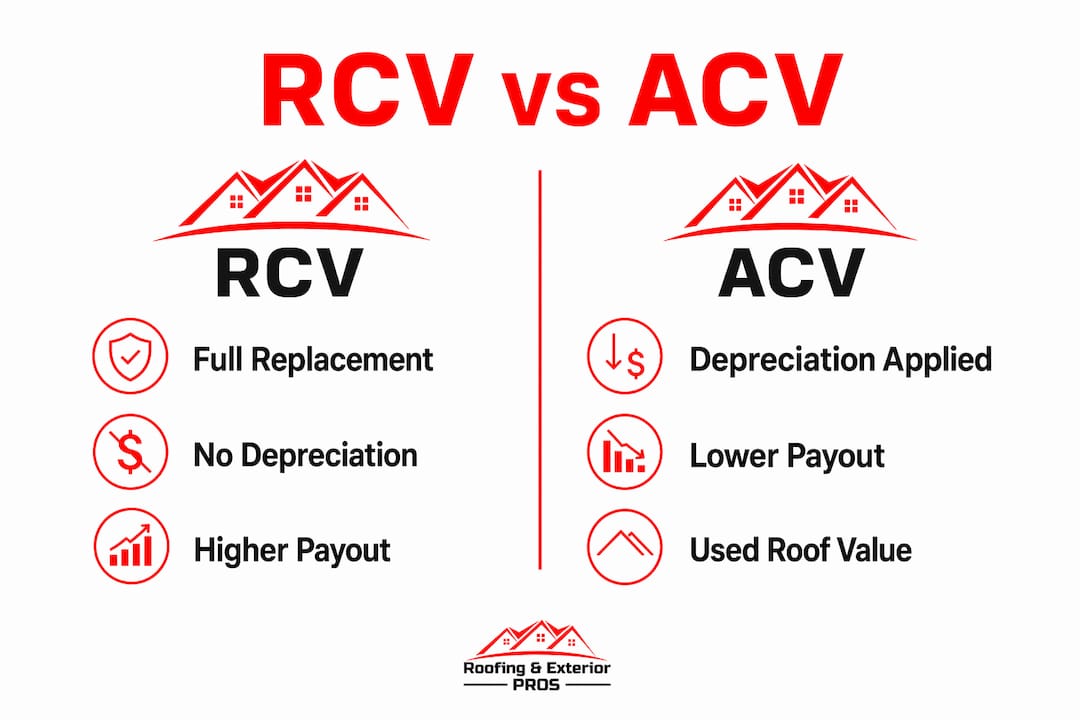

What is the difference between RCV and ACV in roofing insurance?

Replacement cost value (RCV) and actual cash value (ACV) are the two coverage valuation methods that determine how much your insurer pays when your roof is damaged. The difference between them can be tens of thousands of dollars, and your roof’s age and condition directly determine which one applies to your policy.

| Coverage Type | How it works | Best for | Payout example (15-year-old roof, $20,000 replacement cost) |

|---|---|---|---|

| RCV (Replacement Cost Value) | Pays full replacement cost minus your deductible | Newer or upgraded roofs | ~$19,000 (assuming $1,000 deductible) |

| ACV (Actual Cash Value) | Pays replacement cost minus depreciation and deductible | Older roofs, often assigned automatically | ~$5,000 (after 75% depreciation on a roof at 75% of lifespan) |

A real-world example makes this concrete. A 15-year-old roof with a 20-year lifespan has used 75% of its expected life. Under ACV, the payout drops by 75%, leaving you responsible for the gap between what the insurer pays and what the contractor charges. That gap is not a technicality. It is a financial exposure that catches homeowners off guard after a major storm.

Roof upgrades can shift your policy from ACV to RCV coverage, and that shift matters as much as any premium discount. Verifying your policy’s valuation basis with your insurer before investing in an upgrade is a step most homeowners skip, and it is the step that determines whether the upgrade pays off financially. A new roof installed with quality materials and proper documentation is often the trigger that moves a policy from ACV to full RCV status.

Pro Tip: Ask your insurer directly: “Is my roof currently covered under RCV or ACV?” If the answer is ACV, ask what it would take to qualify for RCV. The answer is almost always a documented roof upgrade.

Which roofing materials and certifications lead to premium discounts?

Not every new roof earns a discount. The materials you choose and the certifications you obtain determine whether your insurer recognizes the upgrade as a risk reduction. Here is a ranked breakdown of the upgrades most likely to produce measurable savings:

-

FORTIFIED certification. The FORTIFIED program, developed by the Insurance Institute for Business and Home Safety (IBHS), sets construction standards for wind and hail resistance. In Louisiana and Alabama, FORTIFIED certified roofs receive discounts ranging from approximately 19% to over 40% depending on certification level and location. These are among the largest documented premium reductions available to homeowners anywhere in the country. FORTIFIED certification requires stringent documentation and a formal evaluation process, so working with a certified contractor is not optional.

-

Class 4 impact-resistant shingles. These shingles carry an UL 2218 rating and are specifically tested for hail resistance. Many insurers in hail-prone states like Missouri, Kansas, and Texas offer discounts of 15% to 30% for Class 4 materials. The discount is only applied after you submit the product’s certification documentation to your insurer.

-

Metal roofing. Standing seam metal roofs carry long lifespans, typically 40 to 70 years, and resist wind, fire, and impact better than most asphalt products. Insurers price metal roofs favorably because the long lifespan reduces the frequency of replacement claims and the material’s performance in severe weather is well documented.

-

Wind-rated and fire-rated materials. Class A fire ratings and wind uplift certifications both reduce risk scores. In wildfire-prone regions, a Class A rated roof can be the difference between a standard policy and a surplus lines policy with significantly higher premiums.

The common pitfall homeowners miss is assuming the discount applies automatically. State programs increasingly require formal certification and documentation before any discount is applied. You need to submit the installation date, product warranty, and certification documentation to your insurer directly. Without that paperwork, the upgrade exists on your house but not in your insurer’s underwriting file.

How can roofing upgrades affect insurance premiums over time?

The relationship between roofing upgrades and premium changes is not always immediate. Several timing and process factors shape when and how your insurer adjusts your rate.

- Premium repricing often lags behind the upgrade. Insurance repricing due to roofing upgrades may lag several months post-renovation due to insurer loss adjustment timelines and policy renewal cycles. If you replace your roof in August and your policy renews in January, you may not see the adjusted rate until the following renewal.

- Claims history interacts with roof condition. A single storm claim does not permanently increase your premium, but roof age and condition as enduring risk signals continue to influence your rate long after the claim closes. Upgrading your roof after a claim removes one of the primary risk signals that keeps your rate elevated.

- Proactive reporting accelerates the adjustment. Insurers using aerial imagery may not update your file immediately after a renovation. Submitting your contractor’s invoice, installation date, and material specifications directly to your insurer is the fastest way to trigger a re-rating. You can also learn more about how roof upgrades affect claims and what documentation matters most.

- Underwriting rule changes can affect timing. Some carriers apply new underwriting criteria only at renewal, not mid-term. If your insurer has recently tightened its roof age rules, an upgrade completed before renewal locks in the better rate for the full policy term.

The practical takeaway is this: treat the upgrade and the insurer notification as two separate tasks. Completing the upgrade is step one. Submitting documentation and following up with your agent is step two, and it is the step that actually moves your premium.

Key takeaways

Roofing upgrades reduce insurance premiums by lowering your home’s risk score, shifting coverage from ACV to RCV, and qualifying you for material and certification discounts that insurers apply only with proper documentation.

| Point | Details |

|---|---|

| Roof condition drives pricing | Roofs in poor condition carry 60% higher loss costs, directly raising your premium. |

| ACV vs. RCV gap is significant | A 15-year-old roof under ACV coverage may receive 75% less in a claim payout than under RCV. |

| FORTIFIED certification pays off | Certified roofs in Louisiana and Alabama earn discounts from 19% to over 40% on premiums. |

| Documentation is required | Submitting installation date, warranty, and certification to your insurer triggers the actual rate adjustment. |

| Premium changes lag upgrades | Repricing may not appear until your next policy renewal, so notify your insurer immediately after installation. |

What I’ve learned from watching homeowners leave money on the table

I’ve worked alongside homeowners in the St. Louis area long enough to recognize a pattern. They invest in a quality roof upgrade, expect their insurance bill to drop, and then feel frustrated when nothing changes at renewal. The problem is almost never the roof. It’s the process that follows.

Most homeowners don’t know their policy’s valuation method until they file a claim. By then, the difference between RCV and ACV is no longer an abstract concept. It’s a $12,000 shortfall they weren’t expecting. My honest advice: call your agent before you sign a roofing contract. Ask specifically whether your current roof is covered under RCV or ACV, and ask what documentation the insurer needs to upgrade your coverage status after the work is done.

The second thing I’d push back on is the assumption that any new roof earns a discount. Material choice matters. A standard three-tab shingle replacement on a 22-year-old roof may simply restore your coverage to baseline. A Class 4 impact-resistant shingle installation with proper certification documentation is a different conversation entirely. That’s the upgrade that moves the needle on both your premium and your coverage terms.

Finally, don’t underestimate the value of a local insurance agent who understands roofing. A generalist agent may not know that your insurer offers a FORTIFIED discount or that submitting a specific form triggers a re-rating. An agent with experience in roofing-related underwriting can identify discounts you’d never find on your own. That conversation costs nothing and can save you hundreds of dollars per year.

— Jake

Ready to upgrade your roof and maximize your insurance savings?

At Roofing & Exterior PROS, we work closely with homeowners across the St. Louis metropolitan area to select roofing materials that meet insurer discount standards and to provide the documentation your carrier needs to adjust your rate. We understand the connection between quality installation and insurance outcomes, and we make that process straightforward for you.

Whether you need a full residential roofing replacement with impact-resistant materials or guidance on what your current roof’s condition means for your coverage, our team is ready to help. We provide free inspections and detailed estimates so you can make an informed decision before committing to any upgrade. Reach out to Roofing & Exterior PROS today to schedule your free roof inspection and find out exactly which upgrades will deliver the strongest insurance benefit for your home.

FAQ

How much can a new roof lower my homeowners insurance?

A new roof can reduce your homeowners insurance premium by 10% to 40% depending on your location, the materials used, and whether the installation qualifies for certifications like FORTIFIED. Older roofs already incurring surcharges of 10% to 20% or more will see the largest reductions after replacement.

Does roof material affect insurance premiums?

Yes, roof material directly affects insurance premiums because different materials carry different risk profiles for wind, hail, fire, and water damage. Class 4 impact-resistant shingles and metal roofing typically earn the largest discounts because they reduce the insurer’s expected claim costs.

What is the difference between RCV and ACV for roof insurance?

RCV (replacement cost value) pays the full cost to replace your roof minus your deductible, while ACV (actual cash value) subtracts depreciation from that amount. A 15-year-old roof at 75% of its lifespan can receive 75% less under ACV, making the coverage type a critical factor in your financial protection.

Will my insurance premium drop immediately after a roof upgrade?

Not always. Premium repricing after a roofing upgrade can lag several months due to insurer processing timelines and policy renewal cycles. Submit your installation documentation to your insurer immediately after the work is complete to trigger the adjustment as quickly as possible.

What documentation do I need to get an insurance discount for a new roof?

You need the installation date, contractor invoice, product warranty, and any applicable certification documents such as a FORTIFIED designation or Class 4 impact rating. Proper documentation including certification is critical because insurers will not apply discounts without it, regardless of the quality of the upgrade itself.