Hiring a roofer without knowing how to review roofing contractor insurance certificates is one of the most expensive mistakes a property owner can make. Many homeowners in St. Louis hand over a signed contract after glancing at a Certificate of Insurance, assuming that piece of paper means they are protected. It does not. The certificate only tells you a policy existed on the day it was printed. What actually covers you, or fails to, lives inside the policy itself, in endorsements, exclusions, and language most people never see. This guide walks you through exactly what to check, step by step, so you hire with confidence.

Table of Contents

- Understanding a roofing contractor’s Certificate of Insurance (COI)

- Key elements to verify on a roofing contractor’s insurance certificate

- Understanding additional insured endorsements and coverage gaps

- Step-by-step process to review a roofing contractor’s insurance certificate

- Common pitfalls and how to handle discrepancies in insurance certificates

- Our perspective: The COI is not the finish line

- Work with a contractor who makes verification easy

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| COI is not coverage | A Certificate of Insurance only shows insurance exists, not that claims will be covered. |

| Verify named insured | Confirm the contractor’s legal business name exactly matches your contract on the COI. |

| Check endorsements | Request and review additional insured endorsements to ensure actual liability protection. |

| Beware coverage gaps | Verify both ongoing and completed operations coverage to avoid post-job claim denials. |

| Review regularly | Review certificates at hiring and at each renewal to maintain continuous protection. |

Understanding a roofing contractor’s Certificate of Insurance (COI)

A Certificate of Insurance, commonly called a COI, is a one-page summary document issued by a contractor’s insurance agent. It lists the insurer, the policy numbers, the coverage types, and the effective dates. It looks official. It feels like proof. The problem is that a COI confers no rights on the certificate holder and is issued “as a matter of information only,” as the standard ACORD form itself states.

That language is not fine print buried somewhere obscure. It is printed directly on the certificate. Yet most property owners never read it, and most contractors never explain it.

Here is what a COI actually tells you and what it does not:

- It confirms a policy was in force on the date the certificate was issued

- It summarizes coverage types, limits, and policy numbers

- It does not guarantee the policy is still active today

- It does not show exclusions, conditions, or endorsements that control actual claims

- It does not mean you are named as an additional insured on that policy

- It does not mean a claim you file will be paid

“A roofing contractor’s Certificate of Insurance is not the insurance policy itself. Standard ACORD certificate language states it is issued as a matter of information only and confers no rights on the certificate holder.”

This matters enormously for St. Louis homeowners dealing with storm damage claims. If a roofer causes additional damage to your property during repairs and their insurer denies the claim due to a policy exclusion, your only recourse may be a lawsuit against the contractor directly. Understanding insurance claim best practices before work begins puts you in a far stronger position.

Now that we know what a COI represents and its limits, let us look at what specific details you must check before hiring.

Key elements to verify on a roofing contractor’s insurance certificate

Knowing a COI has limits is only half the battle. You still need to review it carefully, because even as a summary document, it can reveal serious red flags. Homeowners should specifically check that the named insured matches the contractor’s legal entity in the contract, policy effective dates cover the job period, and limits meet contract requirements.

Here is a numbered checklist to work through every time you receive a COI:

- Named insured: The name on the COI must match the legal business name on your contract exactly. “Dave’s Roofing LLC” and “Dave’s Roofing” are not the same entity in the eyes of an insurer.

- Policy effective and expiration dates: Coverage must span the entire project, including any potential delays. A policy that expires mid-project creates a gap.

- Coverage types: Confirm the certificate shows general liability, workers’ compensation, commercial auto, and umbrella coverage as required by your contract.

- Coverage limits: Check that limits meet your contract minimums. For most residential projects in St. Louis, $1 million per occurrence and $2 million aggregate is a reasonable baseline for general liability.

- Certificate holder information: Your name and address must appear in the certificate holder box. This ensures you receive cancellation notices.

The table below summarizes the coverage types you should look for and why each one matters:

| Coverage type | Why it matters for your project |

|---|---|

| General liability | Covers property damage or injury caused by the contractor |

| Workers’ compensation | Covers injured workers so you are not liable |

| Commercial auto | Covers damage from contractor vehicles on your property |

| Umbrella/excess liability | Provides additional protection beyond primary limits |

| Completed operations | Covers defects discovered after the job is finished |

Pro Tip: Ask for the COI before you sign anything. A contractor who hesitates or delays sending it is a contractor worth reconsidering.

For commercial property owners, the stakes are even higher. Review commercial roof insurance verification tips as part of your standard vendor onboarding process. Residential owners can find additional guidance on residential roofing insurance checks that apply specifically to home projects.

With these verification points in mind, let us focus on understanding the critical importance of additional insured endorsements.

Understanding additional insured endorsements and coverage gaps

This is where most property owners get into real trouble. There is a meaningful legal difference between being listed as a certificate holder and being listed as an additional insured. Many homeowners assume these are the same thing. They are not, and confusing them can cost you significantly.

Listing you as a certificate holder does not grant additional insured coverage. Actual coverage requires an additional insured endorsement, which must be verified separately on the actual policy documents.

Here is what each status actually means:

- Certificate holder: You receive a copy of the COI and may receive notice if the policy is canceled. You have no right to file a claim under the contractor’s policy.

- Additional insured: You are named on the policy itself through a formal endorsement. You can file a claim under the contractor’s policy if their work causes you harm.

The endorsement forms matter too. The two most relevant for roofing projects are:

- ISO CG 20 10: Covers ongoing operations, meaning incidents that happen while the roofer is actively working

- ISO CG 20 37: Covers completed operations, meaning defects or damage discovered after the job is done

Many roofing contractors carry ongoing operations endorsements but lack completed operations endorsements, creating a coverage gap after job completion. That gap is exactly when latent defects like improper flashing or inadequate waterproofing tend to show up, often months after the crew has packed up and left.

Request copies of the actual endorsement forms from the contractor’s insurance agent, not just from the contractor. Agents can confirm what is and is not attached to the policy.

Pro Tip: If a contractor cannot produce endorsement documentation within 48 hours, treat that as a serious warning sign. Legitimate contractors with proper coverage have no reason to delay.

Our team at Roofing & Exterior PROS carries full documentation and is always prepared to provide it upfront, because we believe transparency is the foundation of every good project.

Knowing what additional insured endorsements mean, let us examine the practical steps for reviewing and verifying these certificates effectively.

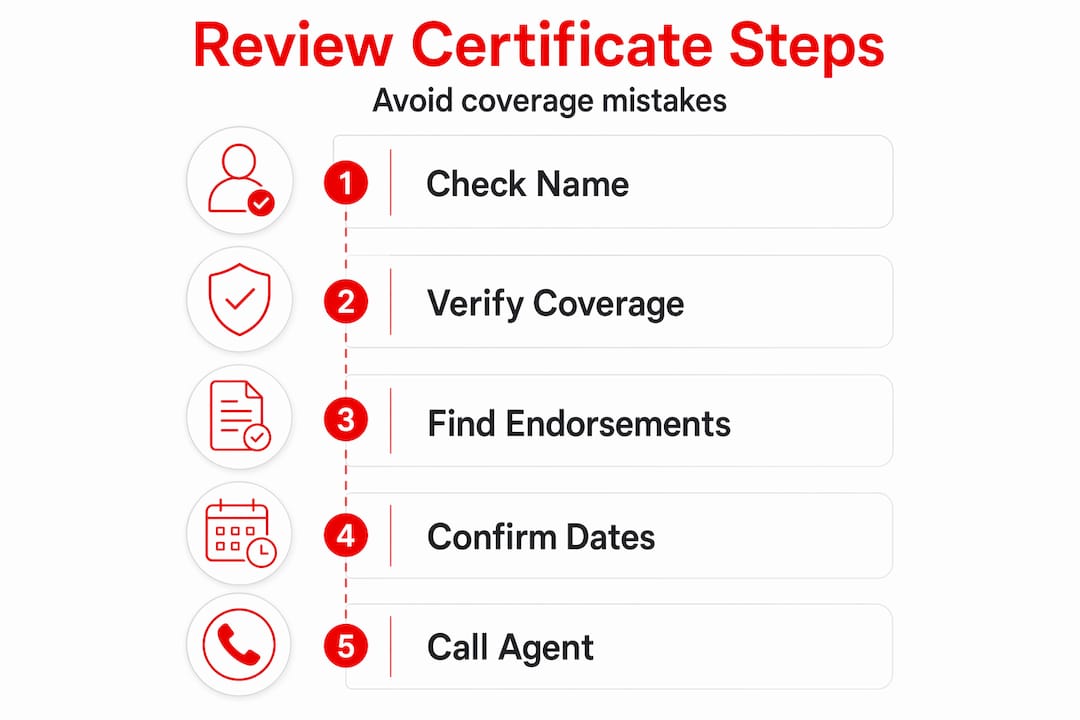

Step-by-step process to review a roofing contractor’s insurance certificate

A clear process removes guesswork and protects you from overlooking something important. COI review involves checking the contract insurance requirements, verifying COI summary fields, and examining actual endorsement documents to ensure full coverage.

Follow these steps before any roofing work begins:

- Pull your contract insurance requirements first. Your contract should specify required coverage types, minimum limits, endorsements, and any special language like “primary and noncontributory” or “waiver of subrogation.” If your contract does not include these, add them before signing.

- Request the COI directly from the contractor’s insurance agent. Agents issue COIs. Receiving one directly from the agent reduces the risk of a doctored or outdated document.

- Check the named insured, dates, and limits against your contract requirements line by line.

- Confirm additional insured endorsements are present and cover both ongoing and completed operations.

- Verify waiver of subrogation language if your contract requires it. This prevents the contractor’s insurer from suing you to recover claim payments.

- Confirm primary and noncontributory language if required. This ensures the contractor’s policy pays first before any of your own coverage is triggered.

- Document every discrepancy and resolve it with the contractor or their agent in writing before signing the contract.

| Review step | What to check | Red flag |

|---|---|---|

| Named insured | Matches contract entity exactly | Any name variation |

| Policy dates | Covers full project duration | Expiration before project end |

| Coverage limits | Meets contract minimums | Limits below contract requirements |

| Additional insured | Both CG 20 10 and CG 20 37 present | Only ongoing operations listed |

| Waiver of subrogation | Endorsed on policy if required | Missing from endorsements |

Pro Tip: Keep a copy of every COI and endorsement document in a dedicated project folder. If a claim arises six months after completion, you will want that paper trail.

You can also review our roofing insurance review steps for additional context on what we require from our own subcontractors and why.

Following these steps helps avoid costly coverage gaps. Next, let us cover common mistakes and how to resolve issues during certificate review.

Common pitfalls and how to handle discrepancies in insurance certificates

Even experienced property managers make mistakes when reviewing roofing insurance documentation. Certificate accuracy issues often arise from entity-name mismatches and missing endorsements, leading to delayed approvals or denied claims.

Watch for these specific pitfalls:

- Named insured mismatch: The COI shows a trade name, but the contract uses the LLC name. Insurers recognize the legal entity, not the trade name.

- Expired policies: A COI printed in January does not mean the policy is still active in August. Always verify current dates.

- Missing completed operations endorsement: As noted above, this is the most common gap in roofing contractor coverage.

- Certificate holder confused with additional insured: This false sense of security leaves you with no claim rights if something goes wrong.

- Inadequate limits: A $300,000 general liability limit may be standard for small handyman jobs but is far too low for a full commercial re-roof.

When you find a discrepancy, do not accept verbal assurances. Contact the contractor’s insurance agent directly and request a corrected COI or written confirmation of the endorsement. If the contractor cannot resolve the issue before work starts, that is a clear signal to pause the project.

Pro Tip: For projects over $25,000 or any commercial roofing work, consider having a licensed insurance professional or attorney review the COI and endorsements. The cost is minimal compared to a denied claim.

If an emergency has already occurred and you need immediate help while sorting out coverage, our team can assist with handling coverage gaps and protecting your property in the meantime.

Our perspective: The COI is not the finish line

After years of working alongside homeowners and commercial property owners across St. Louis, we have seen a pattern that rarely gets discussed openly. Most people treat the COI as the finish line of their due diligence. They get the document, they see the word “insurance,” and they feel protected. The real work, reviewing endorsements, confirming entity names, verifying completed operations coverage, almost never happens.

Here is the uncomfortable truth: contractors who carry inadequate coverage often do not know it themselves. Their agent issued a policy, they paid the premium, and they assume everything is in order. When a claim arises, everyone is surprised. The homeowner is unprotected. The contractor is exposed. And the insurer points to an exclusion that was always there, just never reviewed.

We believe the insurance requirements for roofers should be part of every homeowner’s hiring checklist, not an afterthought. Roofing contractor licensing is important, but a license does not protect your property if a worker falls through your skylight and the contractor’s workers’ comp lapsed two months ago. Verification is not about distrust. It is about protecting an investment that, for most families, represents their single largest asset.

The standard advice is “ask for proof of insurance.” We think that advice stops too short. Ask for the endorsements. Ask for the agent’s contact information. Ask what the completed operations limit is. Those questions separate contractors who carry real coverage from those who carry paper coverage.

Work with a contractor who makes verification easy

At Roofing & Exterior PROS, we understand that trust is built through transparency, and that starts before a single shingle is touched. We are a local, family-owned company serving the St. Louis metropolitan area, and we are fully prepared to provide complete roofing insurance documentation, including endorsement forms, directly from our insurance agent.

We work closely with homeowners and commercial property owners to make sure every project starts on solid ground, with proper coverage in place for both ongoing and completed operations. Whether you need a residential roof replacement, storm damage restoration, or a commercial re-roof, we welcome the questions and the scrutiny. Contact us today for a free inspection and quote, and experience what working with a contractor who values your peace of mind actually feels like.

Frequently asked questions

Does a Certificate of Insurance guarantee that a roofing contractor’s insurance will cover my claim?

No, a COI only confirms that a policy existed on a certain date. Actual claim coverage depends entirely on the policy terms, endorsements, and exclusions, none of which appear on the certificate itself.

What is the difference between being listed as a certificate holder and being an additional insured?

Being a certificate holder means you receive the COI and possibly cancellation notices but have no claim rights. Additional insured status provides actual liability protection through a specific endorsement attached to the contractor’s policy.

Why is it important to verify additional insured endorsements for both ongoing and completed operations?

Ongoing operations coverage protects you while work is in progress, and completed operations coverage protects you after the job is finished. Many roofing contractors carry only the first type, leaving you exposed to post-completion defect claims.

How often should I review my roofing contractor’s insurance certificates?

Review COIs at the start of the project and any time the contractor renews or updates their insurance. COIs should be reviewed at onboarding and at every renewal to confirm continuous, uninterrupted coverage, especially for phased or long-term projects.